The Ultimate 2025 Guide: Using an FHA Loan Calculator to Figure Out How Much House You Can Actually AffordBlog, Finance, How to calculate

Exponential Notation Calculator: The Complete Guide for Scientific Computing in 2025Blog, How to calculate, Math

Why Chipotle is the Ultimate Healthy Fast-Casual Choice (And How to Order Like a Pro)Blog, Health, How to calculate

Home Equity Payment Calculator: The Ultimate Guide to Understanding, Maximizing Your HELOC or Home Equity LoanBlog, Finance, How to calculate

High Yield Savings Account Calculator: The Ultimate Guide to Maximizing Your Money in 2025Blog, Finance, How to calculate

FERS Pension Calculator Your Complete Guide to Federal Retirement PlanningBlog, Finance, How to calculate

Federal Employee Retirement Calculator: Your Complete Guide to Planning a Secure Government Career ExitBlog, Finance, How to calculate

Flight Time Calculator: The Ultimate Guide to Accurate Travel Planning in 2025Blog, Date/Time, How to calculate

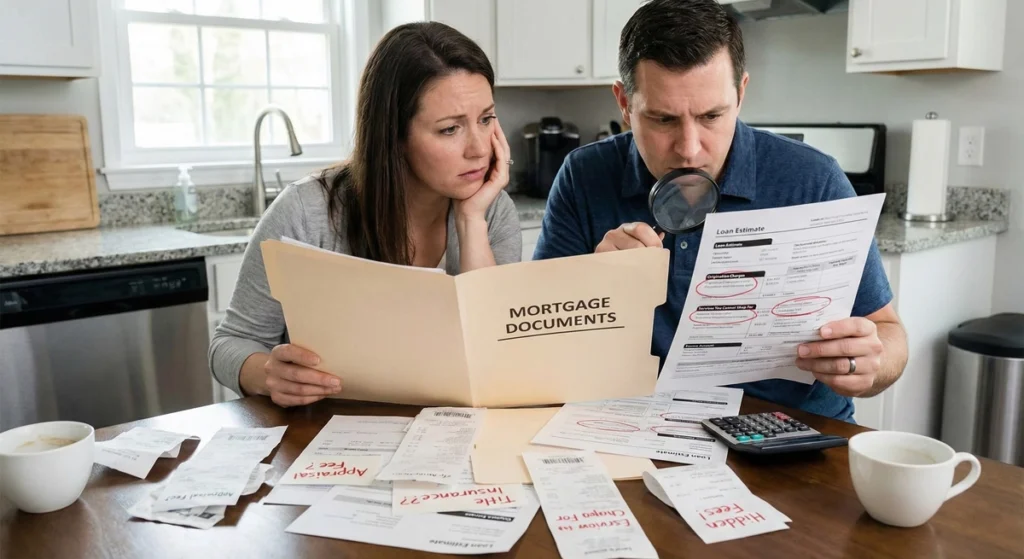

Hidden Mortgage Costs: The Real Price of Homeownership Nobody Tells You AboutBlog, Finance, How to calculate

GPA Calculator: The Ultimate Guide to Academic Performance Tracking in 2025Blog, Education, How to calculate

Intermittent Fasting Made Easy: The 14:10 Method That Actually Fits Your Life (Complete Guide)Blog, Health, How to calculate